Corporate Income Tax Incentives | Indonesian Tax Guide 2025 (3)

tax guide

Tax Guide

Tax guide

Corporate income tax

corporate income tax

Corporate Income Tax

Investing in Indonesia

2025-01-13 09:23:19

Page view:1238

This issue's introduction

Tax incentives

Chapter 1 Corporate Income Tax

Tax Benefits

Tax incentives for investing in Indonesia include:

(1) Enterprises that meet the following conditions at the same time can enjoy the tax exemption period. The tax reduction amount (50% or 100%) and the preferential period (5 to 20 years) are determined according to the size of the investment:

② Develop a new capital investment plan, but have not enjoyed the following benefits:

A. Tax holiday incentives;

B. Tax exemptions for investments in certain areas;

C. Additional deductions for net income from new investments or business expansions in certain labor-intensive industries;

D. Special economic zone corporate income tax incentives.

④ The debt-to-equity ratio stipulated by the Ministry of Finance is met;

⑤ The commitment to implement the investment plan within 1 year after the tax exemption period is approved.

(2) After the tax exemption period ends, the enterprise can still enjoy a 25% or 50% corporate income tax exemption in the next two years based on the investment amount.

(3) Resident enterprises with annual total revenue of less than IDR 50 billion can enjoy a 50% corporate income tax exemption on the part of their taxable income not exceeding IDR 4.8 billion. The annual total revenue refers to the total income obtained by the enterprise through business activities in Indonesia and abroad before deducting all expenses and costs.

(4) The income tax of contractors, consultants and suppliers who are clearly listed in the contract and contract government projects with foreign loans and financial grants can be borne by the government.

(5) Resident enterprises listed on the Indonesian Stock Exchange with a circulating share ratio of not less than 40% that meet the following conditions can enjoy a 3 percentage point reduction in corporate income tax rate, that is, corporate income tax is calculated at a rate of 19%:

① The company has at least 300 shareholders holding more than 40% of the company's issued and paid-in capital;

② Each shareholder holds no more than 5% of the company's issued and paid-in capital;

③ The above conditions are maintained for more than 183 days in a fiscal year.

(6) Domestic taxpayers or permanent establishments (excluding taxpayers who have obtained a business license to provide English and US dollar bookkeeping services) that have fulfilled all tax obligations in the previous tax period can enjoy a tax deferred payment of corporate income tax for a period not exceeding 12 months on the income from the assessed value-added of fixed assets, and the corresponding tax rate for such income is 10%.

(7) Non-profit organizations registered with authorized institutions that conduct education or research and development can be exempted from tax if their surplus is reinvested in infrastructure within 4 years.

The main types of investment are as follows:

① Buildings and educational and R&D facilities, including land purchases;

② Office, laboratory and library facilities;

③ Student dormitories, faculty and staff residences and sports facilities established in formal education institutions.

The above-mentioned surplus refers to the balance of all taxable income other than separately taxed items after deducting the daily operating expenses of non-profit organizations.

(8) Taxpayers who invest in specific fields or specific areas where the state encourages development can enjoy the following tax incentives:

① Investment allowance of up to 30%;

② Accelerated depreciation and amortization;

③ Dividend income tax at 10%;

④ Loss carryforward for no more than 10 years.

A. Conditions for extending losses for 1 year on the basis of the original 5-year carry-forward:

a. New investment in designated industries or designated industries in designated areas;

b. New investment in specific business sectors in industrial zones or bonded areas:

c. Investment in new and renewable energy sources;

d. The taxpayer makes a capital investment of at least 10 billion rupiah in economic or social infrastructure at the business location;

e. From the second year onwards, at least 70% of the raw materials or components are produced locally.

B. Conditions for extending losses for 1 or 2 years on the basis of the original 5-year carry-forward:

a. Provide employment for at least 300 Indonesian workers for 4 consecutive years (extended for 1 year);

b. Provide employment for at least 600 Indonesian workers for 4 consecutive years (extended for 2 years).

C. Conditions for extending the loss carry-forward for 2 years on the basis of the original 5-year period:

a. At least 5% of the capital investment is used for domestic research and development, for product development or to improve production efficiency for a period of 5 years;

b. The investment funds are used to expand the existing business in a specific industry or region, and the funds come from the after-tax income of the fiscal year before the main license for investment expansion is obtained;

c. For investments in specific business areas outside the bonded area, at least 30% of the total project sales come from exports.

(9) According to Presidential Regulation No. 10 of 2021, issued on February 2, 2021, investments in key business activities will be eligible for fiscal incentives in the form of tax exemptions, tax holidays, investment subsidies, and customs incentives such as import duty exemptions on machinery and goods used for industrial development and expansion.

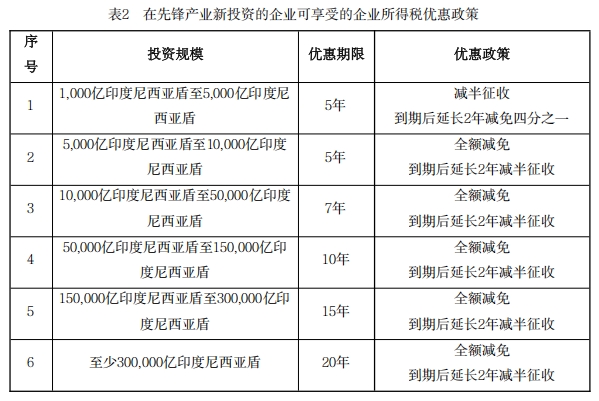

(10) For enterprises making new investments in Pioneer Industry, they can enjoy corporate income tax preferential policies in accordance with the following provisions:

The excitement continues in the next issue...