Taxable Income for Corporate Income Tax丨Indonesia Tax Guide 2025 (4)

tax guide

Tax Guide

Tax guide

Indonesia Investment

Indonesia investment

Corporate income tax

corporate income tax

Corporate Income Tax

2025-01-13 09:26:25

Page view:1207

This issue's introduction

Taxable income

Chapter 1 Corporate Income Tax

Taxable income

Once an accounting principle is adopted, it must be consistently implemented. In practice, almost only small businesses and individual entrepreneurs use the cash basis accounting system.

(1) Taxable income

① Remuneration received or receivable for employment or service provision (including wages, allowances, remuneration, commissions, bonuses, pensions or other forms of remuneration), unless otherwise provided by laws and regulations;

② Lottery proceeds or gifts and rewards obtained as a result of employment and other activities;

③ Business profits;

④ Proceeds from the sale or transfer of property;

⑤ Tax refunds obtained after deducting expenses;

⑥ Interest, including premiums, discounts and compensation for repayment of loan guarantees;

⑦ Dividends of any name and form ;

⑧Royalties;

⑨Rent;

⑩Annuities;

⑪Income from debt forgiveness;

⑫Foreign exchange gains;

⑬Gains on asset revaluation;

⑭Insurance premiums;

⑮Donations received or receivable by charitable organizations from members who are taxpayers engaged in business activities or independent services;

⑯Net wealth increase from untaxed income;

⑰Income from Islamic business;

⑱Compensation income provided by general and tax laws;

⑲Surplus of Bank Indonesia.

Expenditures related to income incurred by resident enterprises and permanent establishments can be deducted before tax, including:

① Costs directly related to economic activities, including:

A. Material cost

B. Employment costs

(including wages, bonuses and other cash expenditures)

a. Food and drinks provided to all employees;

b. Benefits in kind incurred or paid for employment in hardship areas;

c. Benefits in kind required for employees to carry out their work activities;

d. Benefits in kind financed by regional or national revenue budgets;

e. Certain types or conditions of benefits in kind published in regulations issued by the Ministry of Finance.

In addition, medical expenses, social security expenses, housing allowances, etc. borne or paid by employers for employees can be deducted before tax.

a. Medical expenses: hospitalization fees or expenses paid directly by the employer to doctors or hospitals, which are not deductible by the employer and are not taxable by the employee. If the expense is paid directly by the employee to the doctor or hospital and reimbursed by the employer, the expense is deductible by the employer and taxable by the employee.

Medical allowances paid for employee treatment are deductible by the employer and taxable by the employee. The cost of regular employee health checkups under the labor law is also deductible by the employer. Social security expenses: Social security, life insurance, bi-functional insurance and scholarship insurance paid by the employer on behalf of the employee are deductible. Unapproved resident pension fund or non-resident pension fund expenses are deductible by the employer and taxable by the employee.

b. Transportation expenses: Transportation allowances for employees to and from the office are deductible by the employer and taxable by the employee.

c. Accommodation expenses: From 2022, free accommodation provided by the employer is not deductible by the employer and taxable by the employee.

C. Interest

In addition, if there is a special relationship between the parties, debt may be recharacterized as equity. If the funds in a time deposit or other savings are directly or indirectly from a loan or funds from a third party that pays the interest, in this case, if the interest due or paid on this loan is deducted as an expense, while the interest received is from the funds in the time deposit or other savings, the taxpayer may improperly reduce taxable income.

This interest should not be included in taxable income because it has the attributes of final income tax. The above situations should apply:

a. If the loan amount is equal to or less than the amount of funds in the time deposit or other savings, then the entire interest paid or due on such loan is not deductible;

b. If the loan amount is greater than the amount of funds in the deposit or other savings, the portion of the loan interest that can be deducted is the interest paid or payable on the loan amount that exceeds the amount of funds in the time deposit or other savings;

c. If dividends from stocks are exempt from corporate income tax, the interest incurred on the loan obtained to purchase stocks is not deductible. However, non-deductible interest costs can be capitalized as the acquisition cost of such investments and offset against taxable gains on unlisted shares;

d. Final withholding tax on foreign loan interest paid by an Indonesian borrower can be fully deducted as an expense in computing taxable income if the borrowing is actually used for the Indonesian taxpayer’s business.

D. Royalties

E. Travel expenses

F. Waste disposal fees

G. Insurance premiums

H. Advertising and publicity expenses and entertainment expenses as specified in the Ministry of Finance regulations

Entertainment expenses are deductible, but the name and position of the person entertained, as well as the time and place of the entertainment, must be listed. These details must be provided with the annual tax return.

I. Management expenses

There are no specific rules for the deduction of head office expenses and parent company management fees. These amounts are deductible if they meet the general rule that they are necessary to earn, recover or secure income.

However, in practice, head office expenses and parent company management fees may not be deductible based on the following reasons:

a. Non-arm's length transactions between parties with a special relationship;

b. Failure to allocate parent company expenses to a permanent establishment;

c. Taxes other than income tax.

③ Fees paid by pension funds recognized by the Ministry of Finance;

④ Transfer losses of real estate used in economic activities;

⑤ Exchange losses;

⑥ Expenses of R&D activities carried out in Indonesia;

Only R&D expenses incurred in Indonesia and for new technologies or systems that improve business efficiency or processing technology are allowed to be deducted. R&D expenses are divided into three categories:

First, R&D expenses that must be amortized according to the Income Tax Law;

Second, R&D expenses that are daily operating expenses can be deducted in the tax year to which they are related;

Third, expenses other than the above, such as consulting fees, can be deducted according to generally accepted accounting principles.

⑦ Scholarship, internship and training expenses;

⑧ Bad debts written off by taxpayers must meet the following conditions at the same time to be deductible before tax:

A. The bad debt has been included as an expense in the financial statements of the current year;

B. The bad debt details have been submitted to the tax bureau;

C. One of the following circumstances must be met:

a. The bad debt is taken over by the Indonesian National Court or authorized agency and is treated as government receivables;

b. There is a debt relief contract;

c. The bad debt has been disclosed by a specific public institution;

d. The creditor issues a statement of waiver of the debt.

⑩Expenditures for donations to domestic R&D activities as specified by government regulations;

⑪Social infrastructure costs as specified by government regulations;

⑫Expenditures for donations to educational facilities as specified by government regulations;

A. According to Indonesian Government Regulation No. 93 of 2010, donations to national disasters, educational activities, sports activities, research and development work, and the development of non-commercial social infrastructure can be deducted before tax by the donating enterprise, but the following conditions must be met:

a. The amount is not more than 5% of the net income of the donating enterprise in the previous fiscal year;

b. The recipient is a non-related party. If there is a business relationship, employment relationship, service relationship, ownership relationship, etc. between the donor and the recipient, it is considered to have a donation-related relationship;

c. The tax return of the previous year of the donating enterprise shows net income;

d. The donation will not cause the donor to suffer losses in the year in which the donation occurs;

e. The evidence of the donation is attached to the relevant annual tax return;

f. The recipient has a taxpayer identification number, unless the recipient is not a tax subject (such as a foreigner or an embassy employee).

B. Donations can be cash donations or in-kind donations, but donations used to develop non-commercial social infrastructure can only be in-kind donations. The valuation methods for in-kind donations are as follows:

a. The acquisition cost of new assets;

b. The financial book value of old assets;

c. The cost of inventory sales;

d. The actual development cost of infrastructure.

⑬ Reasonable head office expenses;

⑭ Car expenses;

⑮ Other miscellaneous expenses related to the acquisition of income, such as losses caused by theft, embezzlement, misappropriation of public funds or repair and maintenance costs.

(3) Loss compensation

Losses incurred in a particular year can usually be carried forward for 5 years. For investments in certain industries or certain underdeveloped areas, if the taxpayer meets the requirements, the loss carry-forward period is extended to 10 years.

The loss carry-forward period for most mining activity contracts can be extended to 8 years.

(4) Non-deductible items

① Any form of profit distribution;

② Expenses incurred for the benefit of shareholders, partners or investors;

③ Provisions except for the following circumstances:

A. Bad debt reserves of banks and other financial institutions;

B. Bad debt reserves of banks are deductible before tax in the following proportions:

b. Special attention: 5%;

c. Non-standard: 15%;

d. Bad debt: 50%;

e. Loss/bad debt: 100%.

C. The bad debt provision of small rural banks shall be deducted before tax according to the following ratios:

a. Standard: 0.5%;

b. Non-standard: 10%;

c. Bad debt: 50%;

d. Loss/bad debt: 100%.

D. The bad debt provision of infrastructure financing companies shall be deducted before tax according to the following ratios:

a. Standard: 1%;

b. Special attention: 5%;

c. Non-standard: 15%;

d. Bad debt: 50%;

e. Loss/bad debt: 100%.

E. The bad debt reserves of cooperatives engaged in savings and loan activities shall be deducted before tax according to the following ratios:

a. Standard: 0.5%;

b. Substandard: 10%;

c. Bad debt: 50%;

d. Loss/bad debt: 100%.

G. The upper limit of bad debt reserves for consumer finance companies is 5% of the average accounts receivable at the beginning and end of the tax year;

H. The upper limit of bad debt reserves for insurance claims companies is 5% of the average accounts receivable at the beginning and end of the tax year;

I. Insurance reserves for providing insurance services;

J. Guarantee reserves of guarantee institutions;

K. Mining enterprise exploration reserves;

L. Afforestation reserves of forestry enterprises;

M. Industrial waste materials of garbage disposal enterprises Site maintenance reserve;

④ Insurance premiums paid for individuals, excluding insurance paid by the unit as employee remuneration;

⑤ Compensation for work or services in the form of benefits, excluding benefits provided to employees in the form of food and beverages;

⑥ Excessive work remuneration paid to shareholders or other related parties;

⑦ Gifts, assistance or donations provided to others without compensation, except as otherwise provided by the government;

⑧ Corporate income tax expenses;

⑨ Expenses paid for other taxpayers or their relatives;

⑩ Wages paid to members of associations, firms, and partnerships;

⑪ Fines and penalties, including those prescribed by tax laws.

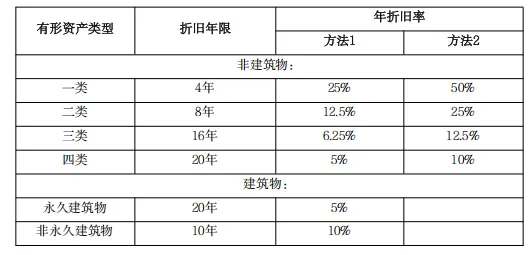

Expenditures on assets and intangible assets with a useful life of more than one year should be amortized or depreciated. Buildings can only be depreciated using the straight-line method. Other assets may be depreciated or amortized using the straight-line method or the declining balance method, and once a choice is made, it should be followed consistently. Intangible assets may also be amortized using the units of production method.

Land is not depreciable, except in certain industries, such as ceramics, roofing and brickmaking.

In general, owners of assets with a useful life of more than one year who use such assets to earn, secure and recover their income are entitled to claim depreciation. The depreciation allowance ends when the asset is no longer used due to gift, inheritance, sale transfer or any other reason (such as fire). Assets that have been repaired or improved are depreciated in the period in which they earn income.

Depreciation of assets under finance leases is not deductible. When the purchase option is exercised, the lessee may treat such assets as depreciable assets.

① Method

Method 1: Expenses incurred on the purchase of tangible assets other than land should be depreciated using the straight-line method over their useful lives;

Method 2: The above tangible assets, except for buildings, may also be depreciated using the accelerated depreciation method at the prescribed depreciation rate over their useful lives.

② Years

Generally speaking, assets are depreciated from the month they are recorded. Depreciation of buildings that are still under construction or assembly begins from the month of completion. However, with the approval of the tax bureau, depreciation may be accrued when the asset is put into use or commercial operation.

All depreciable tangible assets are divided into four categories based on their economic useful lives. Taxpayers must keep records for each asset, listing its category, acquisition/purchase year, acquisition price and related depreciation rate, so that the amount of depreciation to be deducted for each asset can be determined at any time.

From January 1, 2022, if the service life of a permanent building exceeds 20 years, depreciation shall be made based on the actual service life recorded by the taxpayer.

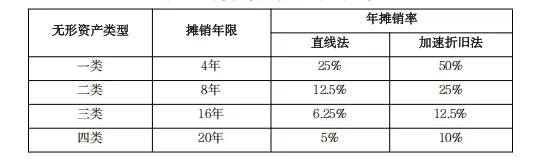

Expenses incurred on the purchase of intangible assets with a useful life of more than one year can be amortized using the straight-line method or accelerated depreciation method; amortizable intangible assets include purchased goodwill and purchased rights, such as construction rights or development rights, pre-commercial operation expenses, such as feasibility studies and trial products, registration costs and research and development expenses, etc.

The useful life of intangible assets and the corresponding amortization rates are as follows:

(6) Tax-exempt income

① Donations, including Zakat received by charitable organizations established or recognized by the government and legal beneficiaries of Zakat (annual charitable donations by Muslims);

② Asset grants received by blood family members with a first-degree kinship relationship, and asset grants received by religious, small business, educational or social organizations and cooperatives specified by the Ministry of Finance (provided that there is no relationship between the business, work, ownership or control of the parties);

③ Inheritance;

④ Assets received by a qualified entity, including cash payments as compensation for shares or investments;

⑤ From 2022, only certain compensation for work or services received in kind or in the form of privileges are tax-exempt;

⑥ Dividends received by domestic enterprises from domestic enterprises;

⑦ Foreign permanent establishments received by resident companies Dividends and after-tax income are tax-free, provided that such income is reinvested in Indonesia or used for business activities in Indonesia (for a certain period of time) and the reinvestment ratio is at least 30% of after-tax profits;

⑧ Payments made by insurance companies to individuals for health insurance, personal accident insurance, life insurance, dual-function insurance and scholarship insurance;

⑨ Fees collected or earned by pension funds approved by the Ministry of Finance;

⑩ Profit sharing of members of limited partnerships (capital is not divided into shares), partnerships, associations, companies and business associations;

⑪ Distribution of retained income of cooperatives;

⑫ Profit sharing of venture capital companies from cooperative entities conducting business and activities in Indonesia, provided that the cooperative entities meet the following conditions:

A. They are small and medium-sized companies, or they conduct activities in the business sectors specified by the Ministry of Finance;

B. Their shares are not traded on the Indonesian Stock Exchange.

⑬Surplus received by registered non-profit organizations in education or research and development, provided that the surplus is invested in the form of educational or research and development infrastructure or equipment within a maximum of 4 years from the date of receipt of the surplus;

⑭Surplus received by registered social and religious institutions, provided that the surplus is reinvested in the form of social and religious infrastructure and equipment or deposited in an endowment fund within a maximum of 4 years from the date of receipt of the surplus.

Next issue continues...